Intro

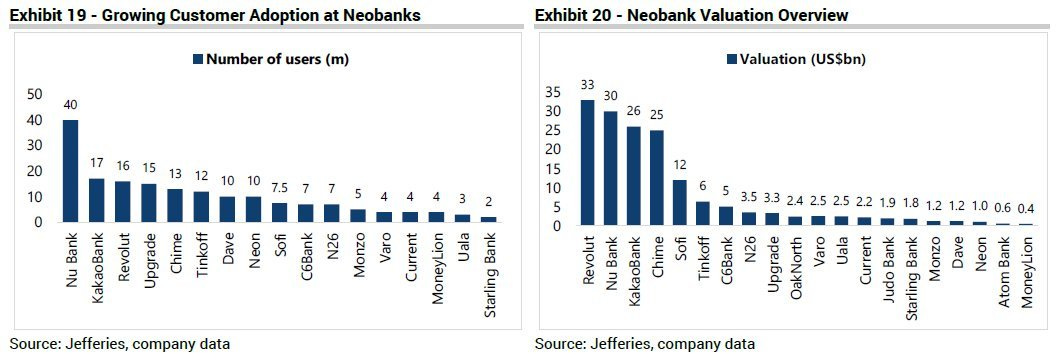

Chances are, if you’re a digital native millennial like me, you’ve either seen ads or currently bank with a neobank (a.k.a challenger bank) like Chime, Dave, Money Lion, Varo, Current, Greenlight, or Marcus. Neobanks are digital-only banks that have no brick and mortar locations and are only accessible via web and mobile applications. Brazil-based Nubank, which recently IPO’d at a ~$41B valuation, is the largest neobank in the world in terms of total number of account holders, boasting over 48M account holders with customers across Brazil, Columbia, and Mexico.

Neobanks have continued to gain in popularity in the United States. They have seen increased adoption due to their digital-first focus and (relatively) customer-friendly features and offerings that are usually tailored to a specific customer demographic. Jeffries projects that by 2025 14% of the U.S population will be account holders of neobanks.

Neobanks are not chartered banks. They’re non-banking technology organizations that offer banking services. In other words, your hard earned cash isn’t sitting in an account earning interest at Chime. It’s sitting at the Bancorp Bank.

Bancorp Bank is Chime’s “Sponsor Bank.” A sponsor bank is a fully-charted bank that can offer full-banking services (deposits, withdraws, transfers etc.), handle compliance, and are approved by the open card-networks such as Visa and Mastercard to issue both debit and credit cards.

The Banking Charter

You might be thinking, “Why do neobanks even need a sponsor bank? Can’t they just get their own banking charter and become a bank themselves?”

They certainly could, and there’s two ways that they could do it. First, they could organize as a de novo bank, which is lawyer speak for starting the process of becoming a charted bank from scratch. Second, if they have the capital to do so, they could acquire an existing bank with a national banking charter.

There are some benefits that come with having a national banking charter. It can lower a bank’s cost of capital and enable them to borrow funds at the fed funds rate, allow them to receive deposit insurance from the FDIC, and as give them the ability to directly access the Federal Reserve’s payment system. However, applying for banking charter can take between 18-24 months according to Deloitte… and a national banking charter doesn’t come cheap. It took Varo Bank three years and cost close to ~$100M to receive their national banking charter from the OCC.

For young venture-backed neobanks, spending freshly-raised capital from investors to pursue a banking charter might not be in their best interest. Instead, they could pursue growth through the acquisition of more account holders. Plus, by not pursuing a banking charter, they can avoid the arduous and expensive application or acquisition processes typically pursued to become a charted bank.

So, unless you have Mortimer and Randolph Duke money, you’re probably not going to start a bank from scratch.

The Shield of Regulation

By partnering with a sponsor bank, neobanks are able to take advantage of a little-known piece of legislation (to those outside of the world of fintech, at least) called the Durbin Amendment.

Enacted in 2011, the Durbin Amendment limits the transaction fees an issuing bank can charge a merchant when a customer uses a debit card, known as interchange fees. Before the Durbin Amendment passed, banks on average were earning $0.44 per debit card transaction. But after the amendment passed, banks were capped at earning $0.21/ debit transaction+0.05% of the transaction size.

However, this cap only applies to banks with >=$10B in assets (think BoA, PNC, Wells Fargo etc.). Banks with <$10B in assets are afforded the right to charge up to 0.80%-1.05% of the total transaction+ $0.15-$0.20. By partnering with a sponsor bank with less than <$10B in assets, neobanks can take advantage of this legislation and earn more from debit interchange revenue.

Which kinds of banks typically have <$10B in assets? Look no further than your local community or regional banks. Common community banks that neobanks and other fintech companies have partnered with include:

Emigrant Bank

Sutton Bank

The Bancorp Bank

Meta Bank

Green Dot Bank

Coastal Community Bank

Beyond the boost in interchange revenue that partnering with a community bank with <$10B in assets provides, there are some additional benefits afforded to neobanks when they partner with a sponsor banks. These include:

Lower capital requirements

Little to no operational risk capital

Limited public and regulatory reporting requirements

Fewer privacy restrictions and no data restrictions

No CRA requirement (Community Reinvestment Act)

No FDIC oversight

A Look Under the Hood

Alright, so you’ve found and partnered with your sponsor bank. Now what? Well now you have figure out how to put together your fancy user-friendly app.

You could build your entire tech stack from scratch, which would be both expensive and time consuming. However, luckily for you, instead of building your neobank’s tech stack from scratch, you can buy the necessary middleware you need to have a fully functioning and secure app.

As a neobank founder you can pick and plug the middleware you need to offer banking services to your customers. Your neobank application can be built on top of a layer of middleware services that handles different necessary core banking functions such as KYC (Know-Your Customer)/AML (Anti-Money Laundering) (Socure and Giact), ACH+ACH fraud and risk management (Orum), account linking (Plaid), direct deposit verification and linking (Atomic).

This middleware sits on top of your Banking as a Service (BaaS) provider. Integrating with a BaaS provider such as Galilio, Synapse, or Stripe Treasury enables neobanks to connect to their sponsoring banks regulated (and often legacy) core infrastructure (FIS, Jack Henry, Termanos) via API.

Before the rise of BaaS providers, neobanks and other fintech companies would’ve had to take on the incredibly burdensome process of signing partnerships with legacy banking institutions and integrating the legacy systems into their own technical stack.

Parting Thoughts

So there you have a it: a small look under the hood of a Neobank.

Neobanks are going to continue to grow in popularity and play major part of the broader opportunity in the world of fintech. I predict that many neobanks will focus on a specific vertical (like construction) and demographic (like higher-income Americans) while taking market share from legacy banking institutions.

The future of banking is opportunity that excites me and I very much look forward to seeing how it plays out.

Thanks for reading! As always, if you have any thoughts, feelings, questions you want to share don’t hesitate to reach out.