Spend and Lend: The Democratization of Credit in the United States.

Spend and Lend: The Democratization of Credit in the United States.

API first companies are empowering credit for all in the United States.

Thanks to the internet, there has never been an easier time to get a personal credit card or corporate credit card for your business.

Consumers can apply online and get approved for a new credit card in a matter of minutes. Small businesses and enterprises can now issue physical or virtual credit cards to their employees or gig-workers at the click of a button (shout-out to Marqeta for making that possible). Founders of tech startups can receive a corporate card without personal guarantees or revenue.

This access to credit (and widespread marketing of credit cards) has caused businesses and consumers to spend like never before. In a study conducted by the Federal Reserve in 2018, credit cards accounted for 34% of all card-based payments. That equates to a total of 44.7 billion transactions at a value of $3.98 trillion, an increase from 33.7 billion transactions with a total value of $3.05 trillion in 2015.

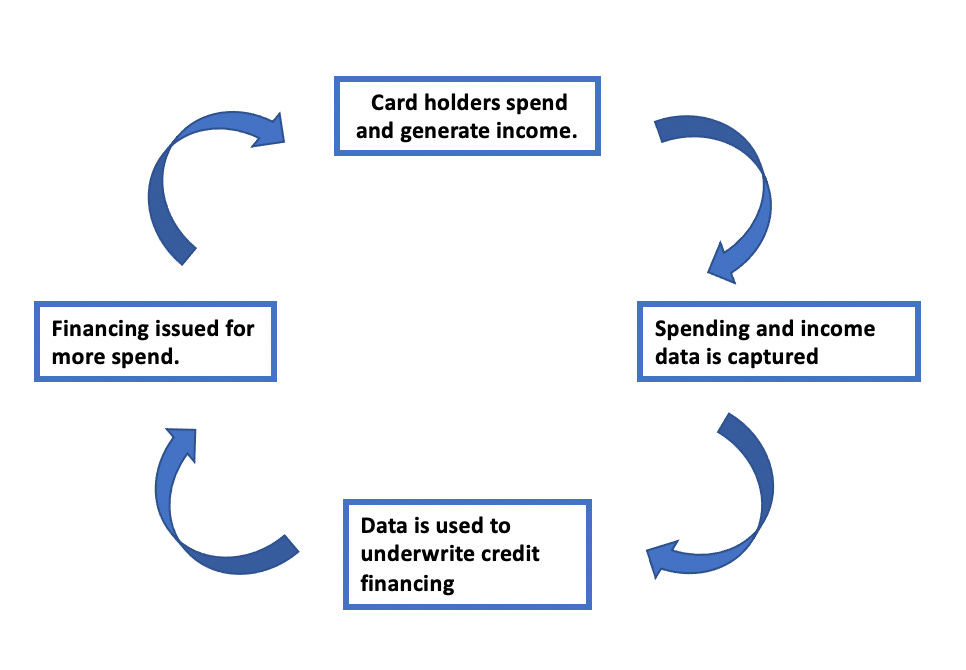

This massive proliferation of credit fueled spending has led to a robust set of spending data that can be captured and disseminated by B2B and B2C fintech focused software businesses. Capturing this data enables software businesses to confidently underwrite consumers and businesses for credit. It’s a process that I’ve coined as spend then lend.

Spend then lend is a catch-all phrase for the process by which B2C, B2B, and B2B2C fintech companies underwrite consumers and businesses for credit based on their spending history, cash in the bank, and income rather than utilizing existing methods like FICO scores, business credit scores, and personal guarantees. Below, I’ll explore the brief history behind credit financing and discuss how software businesses can and will replace traditional FICO and business credit scores through more robust and easily-accessible data.

Underwriting Then and Now

FICO scores (consumer credit scores), are a relatively new concept in the United States, having first been introduced in 1989. Before the introduction of FICO scores by Fair Isaac and Company (FICO), credit approval was largely determined based on the character of the consumer. You could have excellent credit, but banks could still deny your application if they didn’t like something about you. You can see how this was highly problematic and racially inequitable. This eventually led to the shift to creating one method of scoring that wasn’t based on an individual's prejudices. By 1991, all three of the national consumer credit reporting (Equifax, Experian, TransUnion) agencies were selling FICO scores to lenders. In 2020, despite the economic decline due to the COVID-19 pandemic, FICO scores in the United States hit an all-time high in the United States with the average score 710, an increase of 7 points from the previous year's average. The drop in credit utilization and delinquency were the key drivers behind the strengthening of FICO scores.

FICO scores are computed based on the following criteria:

Payment History: The most important piece of criteria in the eyes of lenders is how well you’ve paid your bills on time. The more consistently late you are paying your bills, the bigger the risk you are to lenders.

The Total Amount Owed: Lenders don’t want to see you utilizing a significant amount of your credit that you have available. Doing so makes them nervous about your ability to make payments and your ability to take on more credit.

Utilization: Refers to the number of credit cards that you have open

Credit History: Your credit history refers to how well you’ve been able to manage credit accounts in the past. The longer your credit history and your ability to properly manage credit accounts is a major positive in the eyes of lenders.

Your Credit “portfolio”: Lenders will check to see what additional kinds of credit accounts you presently have open. Examples include student loans, car loans, and other credit cards. If you do a good job paying these off, it’s a positive in the eyes of lenders. But if you have different kinds of credit lines open, it can also be seen as a negative.

It’s important to note that each piece of criteria is weighted differently. Payment History holds the most weight (35%), Total Amount Owed (30%), Credit History (15%), Utilization and Portfolio are both weighted equally (10%).

Like consumers, businesses can be underwritten for credit based off of a credit score with a couple of key differences.

Business Credit Scores have varied ranges pending the reporting agency. 2 of the 3 most popular business credit reporting agencies have a credit score range of 0-100.

Reporting is handled by Dun and Bradstreet which utilizes the PAYDEX Score, Experian Business, and Equifax business.

Unlike personal credit scores, business credit scores are publicly available.

With a strong business credit score, businesses can qualify for more favorable loans from banks and lenders, qualify for lower insurance premiums, and enable businesses to take out loans without a personal guarantee thus protecting the owner/founder’s personal credit score. However, traditionally, many startup and small business founders in order to qualify for a corporate credit card would have to put up a personal guarantee. A personal guarantee essentially just means that if the business is unable to pay off its debt, then the founder(s) and owner(s) of the business are liable to pay off the debt.

Underwriting Credit in the Future

While created to remove the individual personal biases from the credit approval process, FICO and business credit scores can still be considered quite flawed.

What happens if you don't have any credit history? What if you forgot to set that reminder on your phone that let you know your utility bill was due and you didn’t pay on time despite having the funds to do so? What if your vendor fails to report to commercial reporting agencies? What if you’re a pre-revenue startup with $0 in revenue and no customers?

Both scenarios are of course very common in the United States. For context, according to a 2019 report by the Consumer Finance Protection Bureau, nearly 26 million Americans (11% of the population) are considered to be “credit invisible” or those with limited to no credit history. The majority of those that are considered “credit invisible” are Black and Hispanic (15%).

With the rise of the internet and the cloud, consumer financial technology businesses have been able to access more robust consumer financial data from lenders and banks via API’s. Let’s take a look at some notable companies that are providing the connectivity rails that enable both B2B and B2C fintech companies to access your banking and lending data.

Instead of having to make a significant investment upfront in terms of capital, talent, and time to build the necessary infrastructure to integrate with a bank or lender, consumer fintech companies can simply utilize one of these developer friendly API’s instead.

The B2C focused connectivity layer in action.

With the ability to easily access banking and lending data thanks to the rise of the API first businesses, consumer and B2B focused fintech businesses can now tap into data that in the past would’ve been difficult to tap into. Data that they could underwrite instead of FICO and business credit scores.

A great real-life example of this is Petal. Petal is a consumer focused fintech company that offers credit cards to consumers with a lack of credit history. Instead of utilizing a FICO score to determine which consumers qualify for one of their credit scores, Petal has created something called a Cash Score that is instead based off of a consumer’s spending habits, income, and savings. Petal via Plaid’s API can access your banking history and see firsthand your spending, saving, and income history then underwrite you for one of their no annual fee credit cards. Your spending and income history is effectively enabling the level of credit they’re willing to extend to you. As you save, spend, and earn more you can pay off more and you're able to increase your credit limit.

Petal also essentially acts as a gateway for the credit invisible to develop a positive credit history that can enable them to eventually be underwritten for more traditional credit cards from Chase, Capital One, American Express etc.

On the business side, we’ve started to see a new wave of fintechs focused on helping companies receive corporate credit cards but also develop complimentary software solutions that enable those businesses to track and manage their spending like Ramp, Divvy, and Brex. All three drive their revenue from interchange fees and subscriptions on premium feature offerings.

Divvy, Ramp, and Brex will underwrite businesses without a personal guarantee, revenue, or a business credit score. Instead, via an API like Plaid, Divvy, Ramp, and Brex are able to access your businesses financial history and banking data then underwrite you for a credit card based on your cash on hand and your cash-flow. Brex will issue you a corporate card if you have at least $100,000 in cash on hand. This has enabled them to become the favorite corporate cards and spend management tools of small technology companies who may have cash in the bank but are pre-revenue.

The B2B focused connectivity layer in action

Their complimentary value added software that enables you to manage your spending. Divvy’s spend management and budgeting software comes free to companies that utilize Divvy’s corporate credit card and offers some awesome features:

Business purchases can be categorized via a couple taps in their mobile app.

Within their applications, founders and managers can build budgets, alot funds, manage spend within budget.

Receive, View, and pay-off invoices all within their application.

Both Ramp and Brex offer similar functionality with their spend management software as well. It has never been easier to stay on top of cash flow in near real time as a founder of a startup.

What’s next?

Now that B2C and B2B focused fintech’s have easy access to your banking data, spend and lend will become more and more commonplace. We will gradually see a shift away from traditional FICO scores, business credit scores, and personal guarantees and the increased likelihood of more startup and traditional consumer and corporate focused credit card companies underwriting credit based on easily accessible banking and financial data.

These B2C and B2B focused fintech companies powered by API first businesses like Plaid are enabling the future of finance and credit. Combined they can democratize access to credit for 26 million credit invisible Americans and especially those from underrepresented backgrounds. It’s enabling founders and small business owners to tap into credit that enables them to grow their businesses and maintain cash flow. We’re in the very early stages of the democratization of credit in the United States. It’s an exciting opportunity that consumers, founders, small business owners, and investors should all keep their eyes on. Spend and lend is the future.

If you’re interested in discussing credit and or fintech, feel free to send me an email: sean@atentocapital.com